Monetary Cycles (Transformation of Money)

Learn how money flows through the economy, how it grows through investment, and how its value changes over time through inflation and interest.

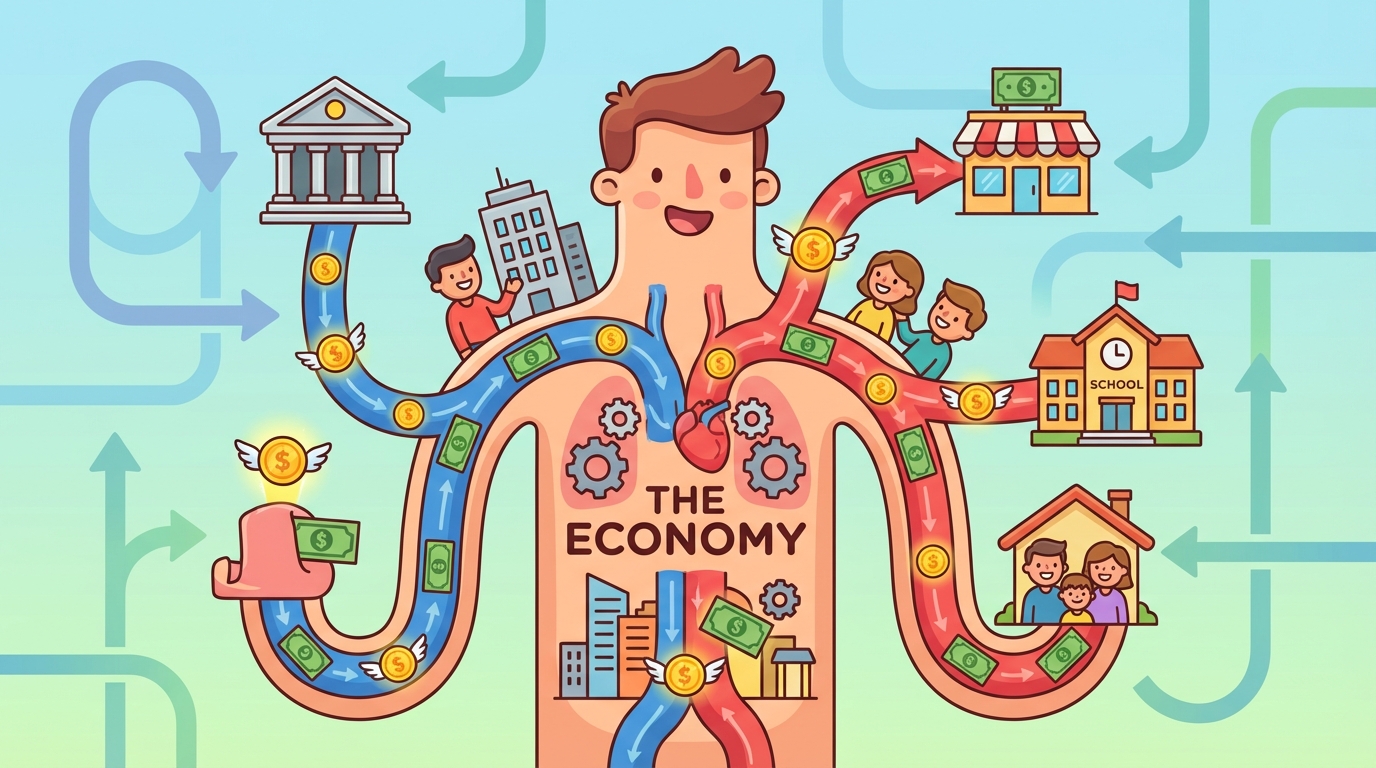

1 Money in Motion: The Economic Heartbeat

Imagine the economy is like a giant body. If people are the cells, then money is the blood flowing through it! 🩸💰 Just like blood needs to circulate to keep you alive, money needs to move to keep the economy healthy.

🔄 The Cycle of Money

Money doesn't just disappear when you spend it. It transforms and travels! This is called the Circular Flow.

👨👩👧👦

Parents work or you do chores to get money.

🛒

You buy a video game. The store gets the money.

👷

The store pays its employees, who then spend that money again!

How Money Changes Form 🦋

Money isn't always coins and paper. Today, it changes shape constantly!

| Form | Description | Example |

|---|---|---|

| Physical Cash 💵 | tangible coins and bills. | Paying $5 for lunch. |

| Digital Money 💳 | Numbers in a computer system. | Tapping a card or using an app. |

Key Facts

2 The Circular Flow Model: Households and Businesses

The Economy is a Circle!

Imagine the economy as a giant, never-ending game of catch. Money flows in a circle between two main teams: Households (people like you and your family) and Businesses (companies that make things).

🏠 Team 1: Households

This is you! Households own the resources. Most importantly, you own your labor (your ability to work).

- 👉 Give: Labor (working at a job) and Money (spending).

- 👈 Get: Income (paychecks) and Goods (stuff you buy).

🏭 Team 2: Businesses

These are the producers. They use resources to make goods and services that we need.

- 👉 Give: Wages (money for workers) and Products.

- 👈 Get: Labor (workers) and Revenue (money from sales).

🔄 How the Cycle Works

It happens in two places called markets:

- Resource Market: You go to work. The business pays you money. (Labor ➡️ Money)

- Product Market: You take that money to the store to buy a video game. The business gives you the game. (Money ➡️ Goods)

The money you spend becomes the money businesses use to pay workers... and the cycle starts all over again! 🚀

Key Facts

3 The Role of Banks: Keeping the Cycle Moving

🏦 Banks: The Heart of the Economy

Have you ever wondered what happens to your money after you put it in a bank? It doesn't just sit in a vault gathering dust! 🕸️

Banks act like the heart of the economy. Just like your heart pumps blood to keep your body moving, banks pump money to keep businesses and families moving. They are the bridge between people who have money (savers) and people who need money (borrowers).

💰 The Saver (You)

When you deposit money, the bank pays you a small reward called Interest. You are technically lending your money to the bank!

- ✅ Your money is safe.

- 📈 Your money grows slowly over time.

🏗️ The Borrower

The bank lends your money to people who need to buy a house, a car, or start a bakery. They pay the bank extra money (Interest) for this service.

- 🚀 They get money now to achieve goals.

- 💸 They pay back more later.

🔄 The Cycle in Action

Imagine Sarah deposits $100. The bank keeps $10 safely in the vault and lends $90 to Mario to buy flour for his bakery. Mario sells bread and pays the bank back $95. The bank gives Sarah a little interest, keeps a profit, and the cycle starts again! 🥖

Key Facts

4 Saving vs. Investing: Transforming Cash into Capital

What do you do with your money? Do you keep it safe, or do you make it work for you? Let's explore how cash transforms into capital! 🚀

🐷 Saving (The Safety Net)

Saving is setting money aside for safe-keeping. It is like putting money in a piggy bank or a standard bank account.

- ✅ Risk: Very Low (It is safe).

- ✅ Access: Easy (You can get it anytime).

- ✅ Goal: Short-term (Buying a video game, emergency fund).

🌱 Investing (The Growth Engine)

Investing is using money to buy things that might increase in value over time. This turns your cash into capital.

- 📈 Risk: Higher (Value can go up or down).

- 📈 Access: Harder (Best left alone to grow).

- 📈 Goal: Long-term (College, buying a house).

The Lemonade Stand Example 🍋

| Action | Outcome |

|---|---|

| Saving | You keep your $10 profit in a jar. Next year, you still have exactly $10. |

| Investing | You use your $10 to buy a better juicer. Next year, you sell twice as much lemonade and make $20! |

Key Facts

5 Compound Interest: How Money Multiplies

Imagine if your money could have babies, and then those babies had babies! 👶💰 That is exactly how Compound Interest works. It is not just magic; it is math!

❄️ The Snowball Effect

Think of a small snowball rolling down a hill. As it rolls, it picks up more snow. The bigger it gets, the more snow it picks up with every turn. Compound interest makes your savings grow faster the longer you leave them alone because you earn interest on your original money PLUS the interest you already earned!

Simple vs. Compound Interest (Starting with $100 at 10%)

| Year | Simple Interest 😐 (Only earns on the $100) | Compound Interest 🚀 (Earns on Total Amount) |

|---|---|---|

| Year 1 | $110 | $110 |

| Year 2 | $120 | $121 +$1 Extra! |

| Year 3 | $130 | $133.10 +$3.10 Extra! |

Key Facts

6 Credit and Loans: Using Tomorrow's Money Today

Have you ever wanted to buy something now but didn't have enough cash? That is where credit comes in! 💳

Think of a loan like a time machine for money. It allows you to use money from your future to buy things today. However, borrowing isn't free. When you pay the money back, you usually have to pay a little extra called interest.

This is the amount of money you borrow. If you borrow $100 to buy a bike, your principal is $100.

This is the 'rent' you pay for using someone else's money. If the bank charges $10 interest, you pay back $110 total!

| Debit Card 🟢 | Credit Card 🔴 |

|---|---|

| Uses money you already have in your bank account. | Uses borrowed money that you must pay back later. |

| No interest fees (usually). | You pay interest if you don't pay the full bill every month. |

| Limit is your account balance. | Limit is decided by the bank. |

Key Facts

7 Inflation: When Money Loses Power

🎈 What is Inflation?

Imagine you have a time machine. If you took $20 back to the year 2000, you could buy a huge feast of pizza and sodas. Today, that same $20 might only buy one small pizza. 🍕

This is called Inflation. It is when prices go up over time, which means your money loses its purchasing power (it buys less stuff!). It's like an invisible balloon expanding the prices of everything around you.

🛒 The Shopping Cart Test

Let's look at how prices change over time for common items. This shows why saving money under your mattress isn't always a good idea!

| Item | Price Then (2000) | Price Now |

|---|---|---|

| Movie Ticket 🎟️ | $5.00 | $15.00 |

| Candy Bar 🍫 | $0.75 | $2.00 |

| Video Game 🎮 | $40.00 | $70.00 |

🤔 Why does it happen?

Inflation usually happens for two main reasons:

- Too much money: If the government prints too much money, cash becomes less rare and valuable. 🖨️💸

- High Demand: If everyone wants to buy the same sneakers but there aren't enough made, the price goes up! 👟

Fun Fact: A little bit of inflation (about 2% a year) is actually considered healthy for a growing economy!

Key Facts

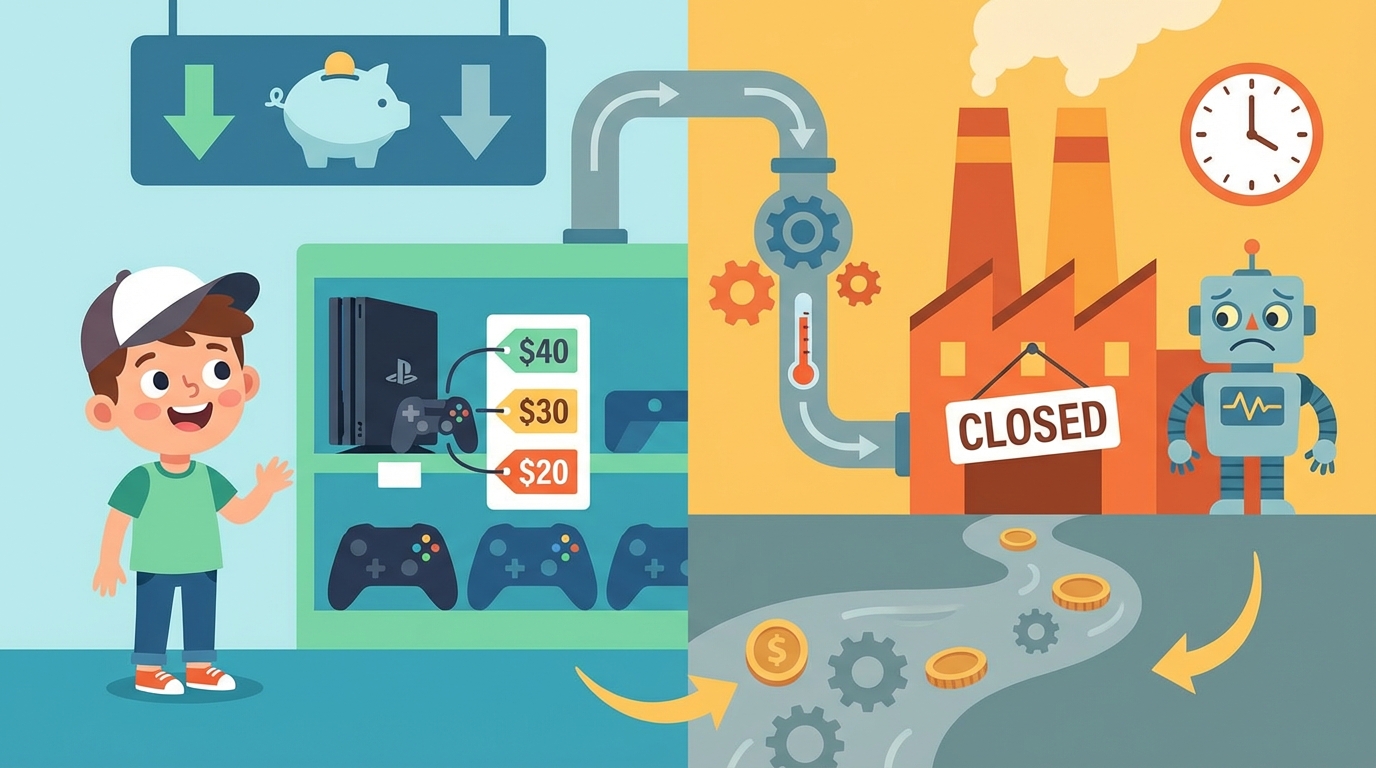

8 Deflation and Stagnation: When the Flow Slows

Imagine walking into a store and seeing that your favorite video game is cheaper than yesterday. Sounds great, right? 🎮 But what if prices kept falling every single day? This is called Deflation, and it can actually be a tricky trap for the economy!

Deflation happens when the general prices of goods and services go down. While cheap stuff seems cool, it causes a problem called the 'Wait and See' effect.

Stagnation is like a traffic jam on the highway of economics. The economy stops growing, businesses don't hire new people, and wages (salaries) stay the same or drop.

The Deflationary Spiral 🌀

When deflation and stagnation mix, it creates a spiral:

- Prices drop because people aren't buying.

- Businesses make less money.

- Businesses pay workers less or cut jobs. 😟

- People have less money, so they buy even less!

🤔 Real World Example: The Tech Wait

Think about smartphones. Sometimes people wait months to buy a phone because they know the price will drop when a new model comes out. Now, imagine if bread, milk, and clothes worked that way. Farmers and factories would go out of business waiting for us to buy things!

Key Facts

9 The Central Bank: Regulating the Supply

Who is the 'Boss' of all banks? Meet the Central Bank! 🏦

While regular banks help people save and borrow, the Central Bank (like the Federal Reserve in the USA) manages the money for the whole country. They don't have savings accounts for you or me; they deal with other banks and the government.

Imagine the economy is a swimming pool and money is the water. The Central Bank controls the faucet to keep the water level just right.

If the economy is slow, the bank adds money (lowers interest rates). This makes borrowing cheap, so businesses build factories and people buy houses!

If there is too much money (Inflation), prices go up too fast. The bank slows the water (raises interest rates) to cool things down.

How Interest Rates Work 📉📈

| Action | Borrowing Money | Result |

|---|---|---|

| Low Rates 📉 | Cheap & Easy | People spend more 🛍️ |

| High Rates 📈 | Expensive & Hard | People save more 💰 |

Real Life Example: If the Central Bank raises rates, buying a new video game console on a credit card becomes more expensive because the bank charges your parents more interest!

Key Facts

10 Key Vocabulary

Master these important terms for your exam:

| Term | Definition |

|---|---|

|

Barter

Trueque |

Trading goods or services directly for other goods or services without using money.

Intercambiar bienes o servicios directamente por otros bienes o servicios sin usar dinero. |

|

Currency

Moneda |

The specific system of money used in a particular country (like Dollars or Euros).

El sistema específico de dinero utilizado en un país determinado (como dólares o euros). |

|

Medium of Exchange

Medio de cambio |

Anything that is generally accepted as payment for goods and services.

Cualquier cosa que se acepta generalmente como pago por bienes y servicios. |

|

Circulation

Circulación |

The movement of money from person to person as it is used for transactions.

El movimiento del dinero de una persona a otra a medida que se usa para transacciones. |

|

Income

Ingresos |

Money received, usually on a regular basis, for work or through investments.

Dinero recibido, generalmente de forma regular, por trabajo o inversiones. |

|

Expenditure

Gasto |

The action of spending funds on goods or services.

La acción de gastar fondos en bienes o servicios. |

|

Savings

Ahorro |

Income not spent on current consumption, kept for future use.

Ingresos que no se gastan en el momento, guardados para uso futuro. |

|

Investment

Inversión |

Using money to purchase assets in the hope that they will generate more money in the future.

Usar dinero para comprar activos con la esperanza de que generen más dinero en el futuro. |

|

Interest

Interés |

The price paid for borrowing money, or the money earned for saving it in a bank.

El precio que se paga por pedir dinero prestado, o el dinero ganado por guardarlo en un banco. |

|

Inflation

Inflación |

A general increase in prices and a fall in the purchasing value of money.

Un aumento general de los precios y una caída en el valor adquisitivo del dinero. |

|

Purchasing Power

Poder adquisitivo |

The amount of goods or services that a specific amount of money can buy.

La cantidad de bienes o servicios que se pueden comprar con una cantidad específica de dinero. |

|

Supply

Oferta |

The total amount of a specific good or service that is available to consumers.

La cantidad total de un bien o servicio específico que está disponible para los consumidores. |

|

Demand

Demanda |

A consumer's desire to purchase goods and services and willingness to pay a price for them.

El deseo del consumidor de comprar bienes y servicios y su disposición a pagar un precio por ellos. |

|

Central Bank

Banco Central |

The national institution that manages a country's currency and money supply.

La institución nacional que administra la moneda y la oferta monetaria de un país. |

|

Economic Cycle

Ciclo económico |

The flow of money between businesses (who pay wages) and households (who buy goods).

El flujo de dinero entre las empresas (que pagan salarios) y los hogares (que compran bienes). |

Time to Practice!

There are 7 questions waiting for you. Questions are shuffled each attempt.

Take the Quiz